Getty Photos

When the Strait Closed

Desk of Contents

When the Strait Closed

The Commodity Bull Market Has Barely Begun

Fourth Quarter 2025 Market Commentary

Surging Uranium Demand Meets a Fragile Provide Base

Silver’s Promote Sign

Copper: Slowing Chinese language Demand Meets Rising Provide

The outbreak of hostilities within the Persian Gulf has already reverberated via international oil markets with exceptional pace. Moderately than try a full survey of supply-and-demand developments in each oil and pure gasoline—subjects we’ll return to in a future letter—we’ll focus right here on the extra quick penalties arising from the efficient closure of the Straits of Hormuz. In our subsequent quarterly commentary we intend to revisit the broader fundamentals: manufacturing developments, depletion dynamics, balancing gadgets, and stock conduct in each the worldwide oil market and U.S. pure gasoline.

As we go to press on March 11, 2026, the Straits of Hormuz stay successfully closed, disrupting the transport of roughly 20 p.c of worldwide oil manufacturing and an analogous share of seaborne LNG provide. In absolute phrases, this represents roughly 20 million barrels per day of crude oil and about 10 billion cubic ft per day of liquefied pure gasoline. By the metric that in the end issues most to power markets—each day bodily quantity—the disruption might already rank as the most important shock the business has ever skilled. The results have been quick: refiners all over the world have begun scrambling for different crude provides, typically at sharply greater costs.

BY THE METRIC THAT ULTIMATELY MATTERS MOST TO ENERGY MARKETS—DAILY PHYSICAL VOLUME—THE DISRUPTION MAY ALREADY RANK AS THE LARGEST SHOCK THE INDUSTRY HAS EVER EXPERIENCED.

China responded rapidly by imposing export restrictions on refined petroleum merchandise on March 11th, in search of to safeguard its personal home provide. As rising U.S. shale manufacturing has dramatically lowered American reliance on imported oil, China has emerged because the world’s dominant crude importer by a substantial margin. A lot of those imports originate within the Persian Gulf and, more and more, from Iran itself. Certainly, in lots of strategic war-game situations involving a hypothetical Chinese language invasion of Taiwan, analysts have lengthy assumed that one of many earliest strikes by adversaries can be an effort to choke off oil shipments to China via the Straits of Hormuz and the Straits of Malacca. In a way, a model of that state of affairs is unfolding at the moment.

Refining margins—so-called crack spreads, which measure the distinction between crude costs and refined product costs—have widened dramatically, reaching ranges not seen since Russia’s invasion of Ukraine in 2022. Brent crude, which had fallen as little as $59.96 per barrel on January 7 and averaged solely about $70 per barrel within the days previous the battle, surged to an intraday excessive of $119.50 on March 9 earlier than retreating to roughly $90 per barrel. Longer-dated Brent futures have moved far much less dramatically. As of this writing, contracts additional out on the curve are buying and selling round $74 per barrel, suggesting that merchants nonetheless view the current disruption as short-term—not less than for now.

In response, the Worldwide Vitality Company convened an emergency assembly of OECD member states. Reviews circulating available in the market counsel that policymakers are contemplating a coordinated launch of as a lot as 400 million barrels from authorities strategic petroleum reserves. If authorized, the discharge would characterize the most important drawdown of strategic shares ever undertaken—greater than double the amount launched following Russia’s invasion of Ukraine in 2022. But even this unprecedented measure would solely partially offset the disruption. After a number of massive drawdowns over the previous 5 years, OECD strategic reserves stand at roughly 1.2 billion barrels, which means the proposed launch would quantity to just about one-third of the remaining stockpile. Even so, it could cowl solely about twenty days of provide misplaced because of the Hormuz closure.

A lot will rely on how occasions evolve within the coming days. The implications are more likely to prolong nicely past the quick disaster. Within the close to time period, consideration stays centered squarely on the Strait itself. A number of producing nations—together with Saudi Arabia, Iraq, and the United Arab Emirates—have already been pressured to curtail subject manufacturing quickly as onshore storage amenities have reached capability. Saudi Arabia does possess one essential benefit: the East-West pipeline, which permits crude to bypass the Persian Gulf totally by transporting it throughout the Kingdom to the Purple Sea. Even so, the pipeline’s capability is roughly 2.5 million barrels per day under Saudi Arabia’s current manufacturing ranges. Different producers within the area don’t have any comparable outlet.

Over the medium time period, the extent of injury to the area’s power infrastructure stays unsure. To date, america and Israel seem to have averted direct assaults on Iran’s oil amenities, presumably to protect the opportunity of post-conflict financial restoration. Iran, in contrast, has reportedly focused storage tanks, pipelines, and refining belongings in Qatar, the UAE, and elsewhere within the area. The obvious logic behind these strikes is easy: by inflicting most disruption on oil markets, Iran might hope to position political strain on america and Israel as power costs rise.

There may be precedent for such ways. In 2019, Iranian-backed Houthi rebels launched a classy assault on Saudi Arabia’s Abqaiq processing advanced, a facility chargeable for processing almost six million barrels per day of crude. Many analysts later instructed the strike had been supposed as a proof of idea—a rehearsal, of types, for extra consequential assaults sooner or later. The Houthis focused stabilization towers and storage tanks with exceptional precision, specializing in parts that could possibly be repaired comparatively rapidly. Saudi Aramco restored the ability to near-full operation inside weeks. Whether or not Iranian forces will show related restraint within the current battle stays uncertain.

The turmoil has unfolded in opposition to a placing backdrop. Initially of 2026, crude oil was arguably essentially the most disfavored main asset class in international markets. Vitality equities accounted for under about 3 p.c of the S&P 500’s market capitalization—barely above their pandemic-era lows. Oil itself traded at document lows relative to gold and near historic lows in inflation-adjusted phrases. Amongst speculative merchants, the dominant technique had more and more been to guess in opposition to the commodity. Web speculative positioning in WTI futures on the NYMEX alternate started the 12 months at its most bearish stage in fifteen years, and gross quick positions had risen to their highest ranges since 2016.

A lot of this pessimism stemmed from the Worldwide Vitality Company’s persistent narrative that the world was going through what it described as the most important oil surplus in historical past. We’ve lengthy taken a unique view. In keeping with the IEA, international oil manufacturing exceeded demand by 2.2 million barrels per day in 2025, with the excess increasing to roughly 3.0 million barrels per day throughout the fourth quarter. If these figures had been appropriate, international inventories ought to have surged. In apply, they barely budged.

OECD inventories elevated by solely about 200,000 barrels per day over the course of 2025—far under what would have been anticipated if the market had actually been oversupplied by greater than two million barrels per day. The discrepancy turns into much more placing within the fourth quarter. As an alternative of constructing by three million barrels per day, because the IEA’s supply-demand stability implied, inventories truly declined by roughly 200,000 barrels per day. The company accounted for the distinction via a statistical class it labels “miscellaneous to stability”—a line merchandise we have now often referred to, considerably irreverently, because the “lacking barrels.” These are barrels that seem to have been produced however neither consumed nor saved. We’ll return to the topic in additional element subsequent quarter. For the second, it’s ample to notice that the oil market could also be far tighter than generally believed.

Towards that backdrop—an already tight market, record-bearish speculative positioning, and now the closure of the Straits of Hormuz—quick masking has been intense. We suspect {that a} substantial portion of the surge towards $120 per barrel mirrored margin calls and the pressured liquidation of speculative quick positions. A number of stories have circulated in current days describing hedge funds shutting down their power buying and selling desks totally, whereas massive bodily buying and selling homes have reportedly raised tens of billions of {dollars} to bolster their margin reserves and dealing capital. It’s troublesome to think about a agency dismantling its power buying and selling operation at such a second until its positions had been severely wrong-footed.

Over the long term, crucial consequence of current occasions might merely be that traders are pressured to look once more at a sector that they had largely ignored. The shale increase supplied an unlimited buffer of manufacturing development throughout the previous decade, however that development is now slowing and in lots of areas turning damaging. In the meantime, a whole technology of market members has grown accustomed to approaching oil from the quick facet. Real oil bulls have turn into a rarity.

For years the prevailing view has been that the oil business belongs to a bygone period—that it represents, in impact, a barbarous relic of the commercial previous. The identical sentiment prevailed towards gold within the late Nineteen Nineties, shortly earlier than the steel launched into probably the most exceptional bull markets in fashionable monetary historical past. It could be that the occasions of the previous a number of weeks will function a reminder that the oil market, nevertheless retro it might typically seem, stays probably the most consequential markets on this planet—and one which traders ignore at their peril.

The Commodity Bull Market Has Barely Begun

Over the previous 12 months we have now begun listening to the identical query with rising frequency: have we already missed the commodity rally? The priority is comprehensible. Gold has surged to document highs, silver has staged one in every of its strongest advances in a long time, and useful resource equities have quietly loved 5 robust years of efficiency. But beneath these headlines lies a curious reality: most commodities are nowhere close to their historic highs. Actually, the information counsel one thing way more shocking. The commodity bull market might not but have actually begun.

THE COMMODITY BULL MARKET MAY NOT YET HAVE TRULY BEGUN.

Out of the forty-two commodities we monitor, solely seven—gold, silver, platinum, copper, tin, tobacco, and beef—had been buying and selling at document nominal highs as of February. The remaining thirty-five commodities had been nonetheless 46 p.c under their historic peaks. When adjusted for inflation, the image turns into much more placing: solely gold trades at an actual all-time excessive, whereas the opposite forty-one commodities stay roughly 73 p.c under their actual peaks.

The broadly adopted Goldman Sachs Commodity Spot Index paints an analogous image. Even after a number of years of rising costs, the index stays 32 p.c under its nominal excessive reached in 2008 and 56 p.c under its inflation-adjusted peak. Such figures hardly resemble the late levels of a commodity increase. If something, they counsel one thing fairly completely different: a bull market which will nonetheless be in its early innings.

On this essay we define the framework that guides our desirous about commodity cycles—what drives them, how they evolve, and the way traders can choose the place we stand inside them at the moment. Our dialogue shall be deliberately top-down. We is not going to dwell on the detailed provide and demand dynamics of oil, copper, uranium, or agricultural markets, nor will we try to forecast inventories or geopolitics. These basic analyses seem elsewhere on this letter.

As an alternative, we start with a less complicated query: why do commodity cycles happen in any respect?

Most traders settle for that commodities are cyclical. Costs rise dramatically, collapse simply as dramatically, and finally get better once more. But comparatively few can clarify why these cycles recur with such exceptional regularity.

In our expertise, the reply lies in one thing far less complicated than most individuals suspect.

COMMODITY CYCLES ARE FUNDAMENTALLY CAPITAL CYCLES.

Commodity cycles are basically capital cycles. A number of years in the past, at our 2022 investor day, the monetary historian Edward Chancellor introduced a compelling evaluation of capital expenditure cycles. Chancellor, broadly considered one of many main authorities on the topic, argued that a few of the most worthwhile alternatives in markets come up in industries which were starved of capital for lengthy intervals of time.

Few industries illustrate this dynamic extra clearly than commodities. To see why, think about the standard commodity cycle. The cycle typically begins with a scarcity. Provide falls wanting demand and costs start to rise. At first producers earn extraordinary earnings, whereas improvement corporations see the worth of their undeveloped initiatives climb dramatically. Ultimately traders take discover. Capital begins flowing into the sector—initially cautiously, after which with rising enthusiasm.

But in contrast to most industries, commodity provide responds solely slowly. Constructing a mine, growing an oil subject, or establishing a liquefaction facility can take a decade or extra. In lots of sectors the delay between funding and first manufacturing stretches ten to fifteen years.

And the timeline is rising longer. Lots of the best deposits have already been developed, forcing corporations to pursue more and more advanced initiatives. Environmental allowing has additionally turn into extra demanding. Baseline environmental research—as soon as uncommon however now routine—typically require years earlier than development may even start.

Whereas the market waits for this future provide, commodity costs steadily proceed to rise. The paradoxical result’s that at the same time as capital pours into the business, costs preserve climbing, for the reason that further manufacturing has not but arrived.

Ultimately, nevertheless, the pipeline of initiatives turns into overwhelming. The market reaches equilibrium whereas an unlimited wave of future provide continues to be beneath development. Traders, emboldened by years of rising costs, both ignore the approaching manufacturing surge or assume they will exit earlier than the downturn arrives. However the brand new provide inevitably seems.

The deficit turns into a surplus. Costs collapse. Initiatives financed beneath optimistic value assumptions turn into uneconomic. Improvement corporations take impairments, and the place undertaking finance is concerned, bankruptcies typically comply with. Traders flee the sector—often vowing by no means to return. What follows is an extended interval of neglect. Capital spending collapses. Exploration budgets shrink. Initiatives are deferred.

Over time, depletion quietly takes maintain. With funding scarce, provide as soon as once more falls wanting demand. Inventories tighten. Costs start to rise. And the cycle begins once more.

FIGURE 1 Typical Commodity Cycle

THE REMARKABLE FACT IS NOT THAT COMMODITY CYCLES OCCUR. IT IS THAT INVESTORS APPEAR DESTINED TO REDISCOVER THEM EVERY GENERATION.

The sample is acquainted throughout commodity markets. The final cycle alone produced a number of placing examples: the growth of Australian iron ore manufacturing, the explosive development of U.S. shale oil and gasoline, and the fast improvement of Indonesian coal exports. In every case, an preliminary scarcity attracted monumental funding that finally produced a glut.

The exceptional reality isn’t that commodity cycles happen. It’s that traders seem destined to rediscover them each technology.

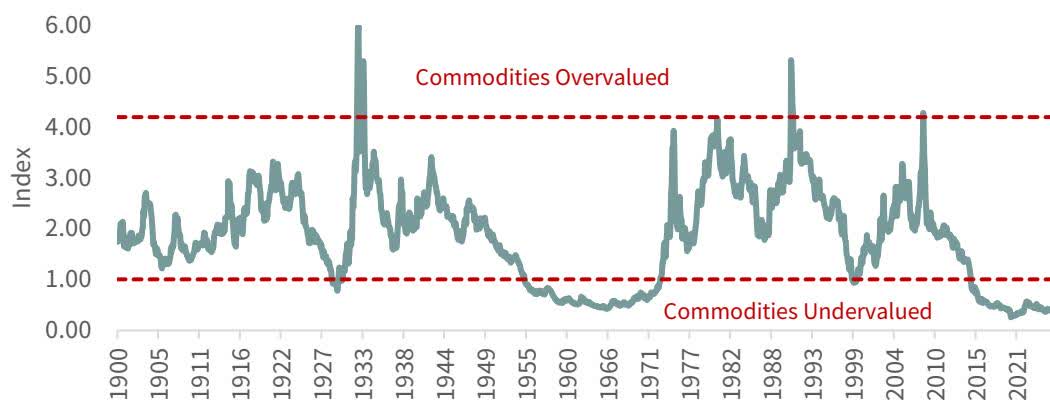

As soon as the mechanism behind commodity cycles is known, the following query naturally turns into: the place are we at the moment? Historical past offers some perspective. Since 1920, there have been three main commodity bull markets: 1929 to 1945, 1969 to 1980, and 1999 to 2011. Every lasted roughly fifteen years and noticed the commodity spot index rise greater than fourfold from trough to peak.

The present bull market started in April 2020. It has lasted just below six years and has produced a achieve of roughly 140 p.c.

Measured in opposition to historic precedent, the current rally seems solely about one-third full, each in period and magnitude. Whereas this comparability is helpful, we imagine an much more highly effective sign exists—one which has quietly predicted commodity turning factors for greater than a century.

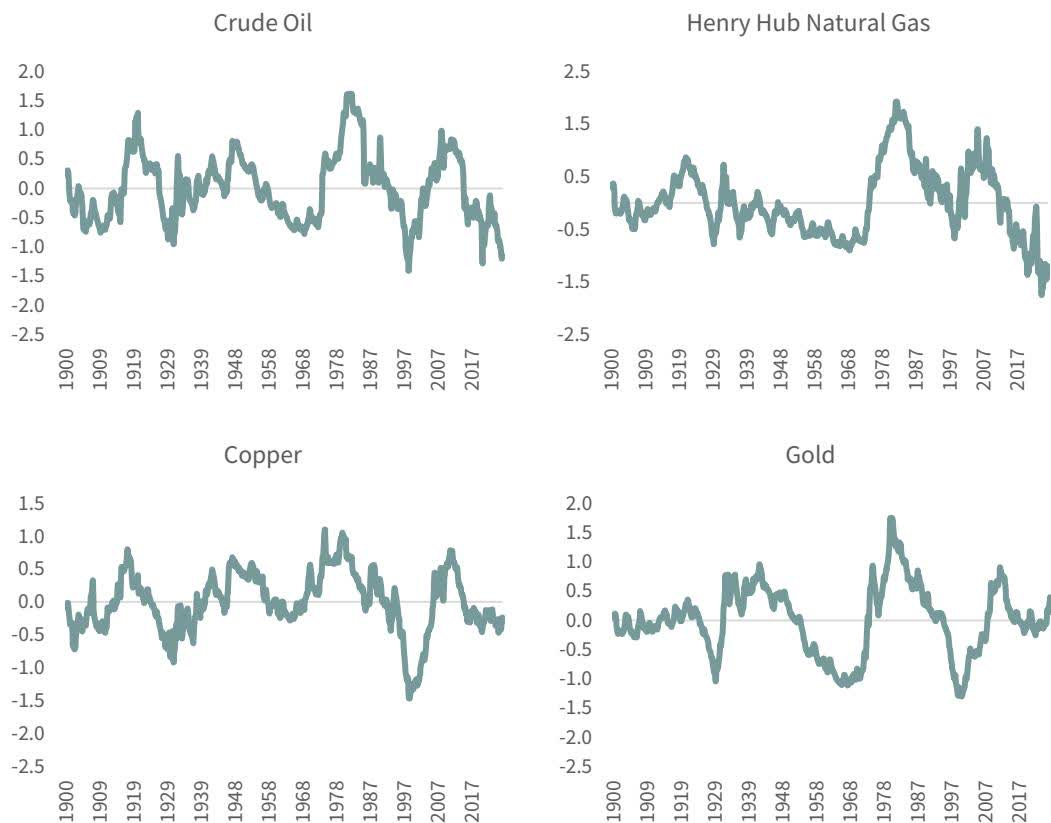

For almost a decade we have now included in our analysis a chart evaluating commodity costs with fairness costs.

The logic behind the ratio is easy. When commodities turn into costly relative to equities, capital floods into the useful resource sector and new provide finally drives costs decrease. When commodities turn into low-cost relative to equities, capital leaves the sector, ravenous the business of funding and setting the stage for future shortages.

FIGURE 2 Commodity Complete Return / Dow Jones Industrial Common

Supply: Bloomberg, G&R Fashions.

In different phrases, the ratio captures the capital cycle itself.

We first encountered this concept in a presentation by Jeffrey Gundlach of DoubleLine. His evaluation started in 1970, the 12 months the Goldman Sachs Commodity Index was created. Curious concerning the longer historic sample, we reconstructed the index utilizing the identical methodology and prolonged the information again to 1900.

The outcomes had been placing. Durations when commodities had been extraordinarily low-cost relative to equities reliably preceded main commodity bull markets. Moments when commodities had been unusually costly relative to equities marked the tip of these rallies.

The chart appeared nearly uncannily predictive. Then a shopper requested a easy query that pressured us to rethink all the things. The shopper’s remark was easy.

Why, he questioned, had been we evaluating a commodity total-return index—which incorporates roll yield and curiosity earnings—to the worth stage of an fairness index?

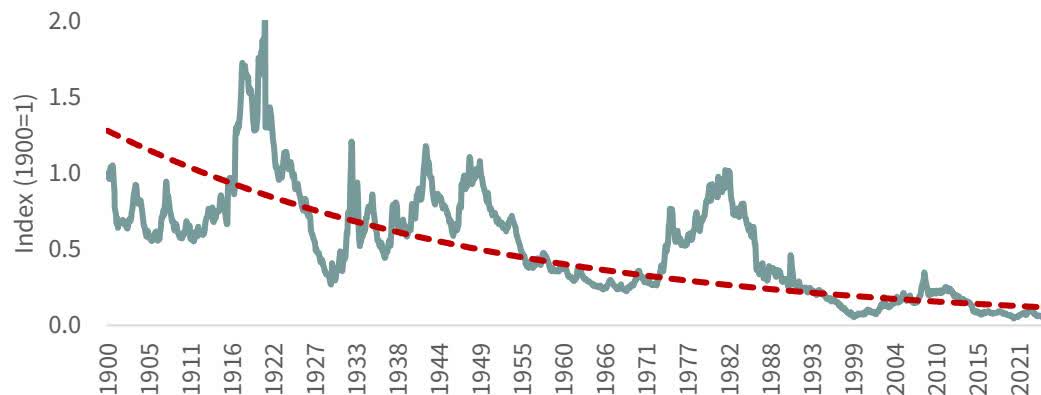

At first the query appeared trivial. Practically each revealed evaluation used the identical method. After we tried to match a commodity spot index with equities, the ratio appeared to break down steadily over time reasonably than oscillate round clear turning factors.

FIGURE 3 Spot Commodity Costs / S&P 500

Supply: David Jacks, Bloomberg, Schiller, G&R.

The whole-return model labored higher, so we adopted it and moved on. But the query lingered. Ultimately we started to suspect that the collapsing development won’t be a flaw within the chart in any respect—however reasonably a clue.

The implication was delicate however highly effective.

Fairness markets take part within the development of the economic system. As productiveness rises and output expands, company earnings rise with it. Over lengthy intervals, fairness costs subsequently develop with each actual financial development and inflation.

Commodities are completely different. Their costs are anchored by the price of bringing new provide to market—the so-called incentive value. Whereas that value might rise with inflation, it doesn’t usually rise with the economic system’s productiveness.

And all of a sudden the puzzle solved itself.

If equities compound at actual development plus inflation, whereas commodities rise primarily with inflation alone, then the ratio between them should decline steadily over time. The inflation phrases cancel, leaving the ratio to fall roughly on the long-term price of actual GDP development.

After we returned to the information with this perception in thoughts, the consequence was placing. The obvious collapse within the commodity-to-equity ratio was not a flaw within the chart in any respect.

It was precisely what financial principle predicted. The ratio certainly fell over a long time by 2-3% per 12 months – inline with long run actual GDP development.

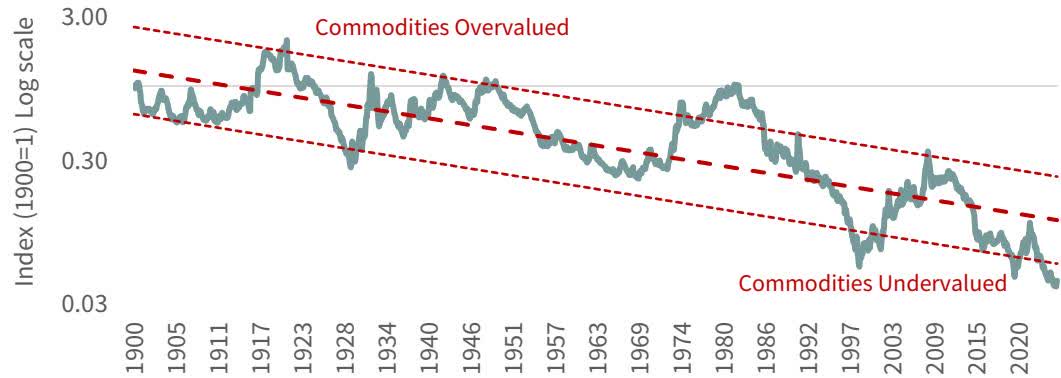

FIGURE 4 Spot Commodities / S&P 500 (Log Scale)

Supply: David Jacks, Bloomberg, Schiller, G&R.

As soon as this structural relationship turned clear, the answer was easy. By eradicating the long-term development development, we may isolate the cyclical fluctuations pushed by the commodity funding cycle. The ensuing detrended commodity-to-equity ratio reveals the true rhythm of commodity markets: lengthy intervals of capital hunger adopted by waves of funding and oversupply. And when seen via this corrected lens, the present sign is extraordinary.

TODAY, COMMODITIES ARE ONCE AGAIN TRADING NEAR THE LOWEST LEVELS RELATIVE TO EQUITIES OBSERVED IN MORE THAN A CENTURY.

Right this moment, commodities are as soon as once more buying and selling close to the bottom ranges relative to equities noticed in additional than a century. This excessive undervaluation helps clarify why investor curiosity—and extra importantly investor capital—has remained scarce throughout the extractive industries. When commodities underperform equities for lengthy intervals, capital naturally flows elsewhere. But historical past reveals that at the moment’s capital drought inevitably turns into tomorrow’s provide scarcity.

By our new measure, commodities at the moment are literally cheaper relative to equities than they had been on the depths of the pandemic panic in 2020. The ratio stands close to the degrees noticed in 1929 and never far above the historic low reached in 1999 throughout the top of the know-how bubble. Moderately than signaling the tip of a commodity increase, the information counsel the other. The commodity bull market might not but have actually begun.

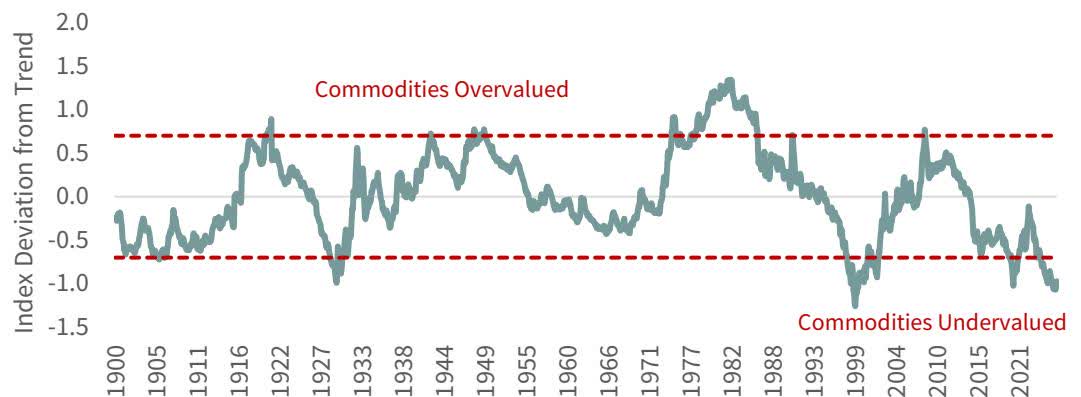

FIGURE 5 Spot Commodities / S&P 500 (Detrended)

Supply: David Jacks, Bloomberg, Schiller, G&R.

Making use of the identical evaluation commodity by commodity reveals clear variations inside the sector. Vitality commodities seem by far essentially the most undervalued. Pure gasoline presently ranks within the 99.fifth percentile of historic undervaluation, oil within the 97.fifth percentile, and coal within the 94th percentile relative to equities. Agricultural commodities and bulk supplies additionally seem attractively priced.

Treasured metals, in contrast, now sit within the higher quartile of their historic valuation vary relative to equities. Their robust efficiency over the previous 12 months helps clarify why we have now lowered our publicity to precious-metal equities in current months.

But even this management sample suits the historic script. Commodity bull markets are likely to comply with a surprisingly constant sequence. Treasured metals typically lead the early levels of the cycle, responding first to financial instability and declining confidence in monetary belongings. Vitality markets usually assume management within the center part of the rally as tightening provide situations collide with robust international demand. Treasured metals steadily regain management close to the tip of the cycle when inflationary pressures attain their peak.

Considered via this historic lens, the current surge in gold and silver seems much less like the tip of a commodity increase than the closing scene of its first act. Ultimately the current commodity cycle will run its course, simply as its predecessors did. To estimate the place that peak may lie, we examined the valuation ranges reached at earlier cycle highs.

If the commodity-to-equity ratio had been to return merely to the eighty fifth percentile of its historic vary—just like the peaks reached in 1920, 1945, and 2011—the implications for commodity costs can be dramatic.

FIGURE 6 Particular person Spot Commodity / S&P 500 (Detrended)

Supply: David Jacks, Bloomberg, Schiller, G&R

Even beneath conservative assumptions for fairness market efficiency, the commodity spot index would wish to rise three- to five-fold from at the moment’s ranges. Oil costs would probably improve four- to six-fold, whereas U.S. pure gasoline may require a nine- to twelve-fold advance to achieve comparable valuation ranges. These numbers might sound extraordinary. But they merely characterize what can be required for commodities to return to the higher finish of their historic valuation vary relative to equities.

With gold making headlines and precious-metal shares dominating the dialog, it’s simple to imagine the commodity rally has already run its course. Historical past suggests in any other case.

Commodity bull markets are likely to final greater than a decade. The present cycle is just a few years outdated. Relative valuations stay close to historic lows, and capital funding within the sector stays depressed.

Traders ready for decrease costs earlier than coming into the useful resource sector might uncover that these costs by no means arrive. In commodity cycles, the best mistake is never shopping for too early.

It’s realizing—too late—that the cycle has already begun.

INVESTORS WAITING FOR LOWER PRICES BEFORE ENTERING THE RESOURCE SECTOR MAY DISCOVER THAT THOSE PRICES NEVERARRIVE.

Fourth Quarter 2025 Market Commentary

Commodity developments that had taken maintain within the first three quarters of the 12 months continued with uncommon power into the fourth. Metals—the strongest performers in each the second and third quarters—prolonged their advance. Main the cost as soon as once more had been the valuable metals, with silver, gold, and the platinum group metals all posting outsized beneficial properties. Silver was the standout, surging 51% throughout the quarter. Platinum and palladium every rose greater than 28%, whereas gold superior 13%. Copper additionally continued its spectacular climb, gaining one other 17% within the fourth quarter and ending the 12 months up a placing 41%. Provide disruptions at two of the world’s largest mines—Grasberg and Kamoa-Kakula—added additional tightness to an already strained copper market.

Outdoors of metals, investor curiosity remained muted and costs usually languished. Oil markets continued to float decrease because the Worldwide Vitality Company doubled down on its bearish outlook for 2026. The IEA initiatives that oil demand will once more disappoint whereas provide continues to surge—primarily repeating the state of affairs it had projected for 2025. But lots of the company’s earlier forecasts, significantly these centered on quickly rising international inventories, have didn’t materialize. Even so, the IEA’s persistently bearish projections—each quick and long run—have solid a deep pessimistic shadow over international oil markets. Oil costs slipped one other 7% throughout the quarter and completed the 12 months down almost 20%. Reflecting this deeply damaging sentiment, the power sector’s weighting inside the S&P 500 stays under 3%, a stage briefly reached solely throughout the depths of the COVID-related panic in April 2020. The lone vibrant spot inside power got here from North American pure gasoline, the place costs superior almost 15% in response to an early burst of chilly climate in December.

Outdoors of power, grain costs had been blended, coal costs continued to agency, and uranium costs had been largely unchanged.

Reflecting the weak spot throughout power markets, the oil-heavy Goldman Sachs Commodity Index slipped modestly throughout the quarter, declining 0.3%. In contrast, the Rogers Inter-national Commodity Index—which carries higher publicity to metals and agricultural commodities—rose almost 3%.

Pure useful resource equities, on common, modestly outperformed the broader market. The S&P North American Pure Useful resource Sector Index, closely weighted towards large-cap power corporations, gained 3.1% throughout the quarter. The S&P World Pure Assets Index, which has higher publicity to metals and agricultural producers, rose 6.6%. By comparability, the S&P 500 Index superior 2.4%.

Treasured Metals

Main the commodities advanced within the fourth quarter was silver. Its roughly 50% advance made it the best-performing commodity of the interval. For the 12 months as an entire, silver’s efficiency was much more exceptional, rising greater than 140%—a achieve rivaled solely by platinum. Gold additionally continued its advance throughout the quarter, climbing 13% and ending 2025 up roughly 65%.

Treasured metals equities likewise remained among the many market’s strongest performers. The VanEck Gold Miners ETF (GDX) rose 12.3% throughout the quarter, whereas the World X Silver Miners ETF (SIL) superior almost 17%. Over the complete 12 months, gold and silver equities had been clear market leaders, surging roughly 140% and 166%, respectively.

In final quarter’s letter, we famous that if silver’s rally continued, it may generate a strong promote sign for gold. Since then, silver costs have climbed one other 50%, and we imagine that sign has now been triggered—suggesting that, not less than within the quick time period, traders ought to think about lowering their publicity to gold.

Over the previous fifty years, silver has staged dramatic “catch-up” rallies relative to gold on solely a handful of events, and we imagine the market has now skilled a fifth such episode. In every prior occasion—1973, 1979, 2011, and 2020—the surge in silver in the end marked an essential turning level. Gold, silver, and their associated equities quickly entered both a pointy correction inside an ongoing bull market or an outright bear market.

Since bottoming in April of final 12 months, silver has surged almost 220%, surpassing the magnitude of the catch-up rallies seen in 1973 (up roughly 150%), 2011 (up about 175%), and 2020 (additionally close to 175%). The one comparable transfer occurred in 1979, when silver likewise superior roughly 220% in a closing explosive rally—one which in the end signaled the tip of the good gold bull market and the start of a two-decade bear market.

For traders working beneath efficiency constraints, we suggest lowering publicity to each gold and silver equities and recycling a portion of these earnings into oil-related investments. By our evaluation, oil at the moment represents the most affordable main asset class on this planet. Retail traders, in contrast, might want to keep their treasured metals publicity and use any weak spot that develops so as to add to positions over time.

Within the gold and silver part that follows, we look at each the bullish and bearish forces now shaping the valuable metals markets. We’ll focus on in higher element the essential message being despatched by silver’s extraordinary rally and why we imagine it has triggered a significant short-term promote sign for gold.

Platinum Group Metals

Platinum group metals continued their highly effective advance throughout the fourth quarter. Platinum and palladium costs every surged roughly 28%, whereas rhodium rose 19%. For the 12 months as an entire, PGMs ranked among the many strongest-performing commodities. Platinum costs climbed roughly 125%, palladium rose 80%, and rhodium superior almost 100%.

Equities tied to the PGM sector additionally carried out strongly. Valterra—the previous Anglo American Platinum (ANGPY)—together with Impala Platinum (IMPUY) and Sibanye-Stillwater (SBSW) gained 19%, 23%, and 27%, respectively, throughout the quarter. Over the complete 12 months the beneficial properties had been much more placing: Valterra and Impala rose roughly 200% and 240% in U.S. greenback phrases, whereas Sibanye-Stillwater surged almost 330%.

Though the surge in gold and silver costs undoubtedly contributed to the energy in platinum group metals throughout the quarter, two essential developments materially improved the basic outlook for PGMs. The prevailing bear case for these metals has lengthy rested on the belief that electrical automobile penetration would speed up quickly, resulting in a gentle decline in inner combustion engine (ICE) automobile gross sales. As a result of roughly 65% of platinum group steel demand comes from auto-catalysts, many analysts concluded that PGM consumption would face a persistent and structural decline.

Latest coverage developments, nevertheless, counsel that this narrative could also be unraveling extra rapidly than beforehand anticipated. In america, the Trump administration—working with congressional approval—has repealed California’s authority to impose stricter automobile emissions requirements beneath the Superior Clear Automobiles II regulation. That rule had mandated that 100% of latest passenger automobiles bought in California be zero-emission by 2035, a framework that seventeen different states had indicated they’d comply with. The repeal represents a major setback for efforts to speed up the phase-out of inner combustion engine automobiles in america.

The administration has additionally rolled again the Biden-era Company Common Gas Economic system (CAFE) requirements from a deliberate 50 miles per gallon to 34.5 miles per gallon. The earlier goal—scheduled to take impact by 2031—was broadly seen by the auto business as a particularly aggressive customary that might have pressured producers to shift a good portion of their manufacturing towards electrical automobiles. Decreasing the CAFE requirement successfully removes what many had seen as a “backdoor” EV mandate. As well as, the administration has repealed the $7,500 federal tax credit score for brand new electrical automobile purchases and eradicated funding for the Nationwide Electrical Automobile Infrastructure (NEVI) charging program.

Lastly, the administration has ended the long-standing apply that allowed automakers to commerce Zero-Emission Automobile (ZEV) credit. Underneath the earlier system, corporations that produced solely electrical automobiles—most notably Tesla—generated massive portions of credit that would then be bought to producers falling wanting their EV manufacturing targets, permitting them to keep away from regulatory penalties. In impact, the system functioned as an oblique subsidy for EV producers. With the elimination of the ZEV credit score program, this mechanism has now been dismantled.

A second essential improvement occurred in Europe. On the finish of 2025, the European Fee signaled a major shift in its automotive coverage, transferring away from the beforehand proposed strict ban on inner combustion engine (ICE) automobiles towards a extra versatile framework geared toward preserving Europe’s home auto business. The EU has now proposed adjusting its prior mandate of 100% zero-emission automobile gross sales to a extra pragmatic goal of a 90% emissions discount. Though not explicitly acknowledged, stepping again from a full ICE ban by 2035 displays a rising recognition that forcing customers towards electrical automobiles too quickly may produce severe unintended penalties—together with the potential erosion of Europe’s car manufacturing base.

A lot of the bearish narrative surrounding platinum group metals has been constructed on the belief that inner combustion engines had been destined for fast decline. As our readers know, we have now lengthy disagreed with that view. Now that each america and Europe have begun to unwind insurance policies designed to speed up the phase-out of ICE automobiles whereas closely subsidizing electrical automobiles, we imagine demand forecasts for PGMs will have to be revised meaningfully greater from at the moment’s extraordinarily pessimistic ranges.

In our view, the extended bear market in platinum group metals was constructed on a flawed narrative—one that’s now starting to be rewritten. As that reassessment unfolds, we imagine the bull market in PGMs is simply in its early levels and will prolong for a few years.

Copper and Base Metals

Base metals, led by copper, had been robust performers throughout the fourth quarter. Copper costs rose 17% throughout the interval and completed the 12 months up a formidable 41%. Regardless of a number of bouts of volatility—largely tied to shifting tariff bulletins from the Trump administration—copper markets proved remarkably resilient. Aluminum adopted with a 12% achieve throughout the quarter, whereas nickel costs additionally moved greater. Zinc was the lone base steel to say no, falling barely by lower than 1%.

Base steel equities had been equally robust and considerably outpaced the broader market. Copper mining shares, as measured by the COPX copper inventory ETF, rose 20% throughout the quarter, whereas the XBM base metals fairness ETF superior 17%. For the complete 12 months, the beneficial properties had been much more dramatic: the COPX ETF surged almost 90%, and the XBM ETF climbed greater than 50%, making base steel equities a few of the strongest-performing useful resource shares of the 12 months.

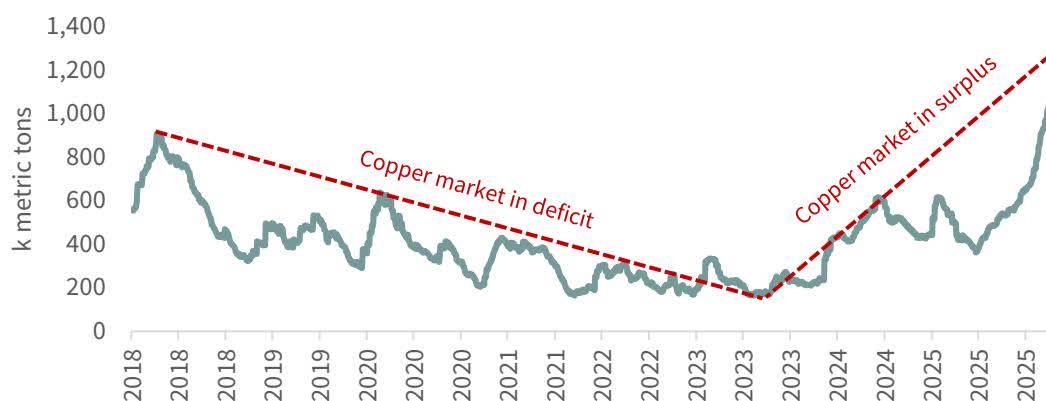

Copper continues to command the market’s consideration, and bullish sentiment towards the steel stays widespread. In earlier letters we famous that we had been short-term bullish on copper whereas sustaining a impartial longer-term outlook. We’ve now shifted that short-term view to a extra bearish stance. The reason being easy: our modeling, mentioned intimately in earlier letters, means that the copper market has moved again into surplus—a shift that’s now clearly mirrored within the persistent rise in inventories held on the main buying and selling exchanges.

Copper inventories on the three main exchanges—Shanghai, the London Metallic Trade, and COMEX—have now exceeded ranges final seen in 2013, when copper costs had been round $3.20 per pound and already starting to say no. After peaking close to 940,000 tonnes in the summertime of 2013, copper costs fell roughly 35% over the next two years, finally bottoming under $2.00 per pound in January 2016.

Right this moment, alternate inventories have risen nicely past these earlier ranges, reaching roughly 1.2 million tonnes—an quantity final noticed in 2003, when copper traded under $0.90 per pound. Even after adjusting for greater international consumption, these inventories characterize roughly 17 days of worldwide copper demand, putting them within the high 20% of observations over the previous thirty years. The final time inventories lined roughly 17 days of consumption—again in 2018—copper costs averaged round $2.90 per pound.

We focus on the newest developments in international copper provide and demand in higher element within the copper part that follows. Our modeling strongly means that the copper market has entered a protracted interval of surplus—a conclusion now strengthened by the regular and important rise in alternate inventories.

Oil

Oil costs continued to float decrease throughout the fourth quarter, declining a further 7%. For the 12 months as an entire, oil exhibited depressing efficiency, falling almost 20%. Oil-related equities fared considerably higher. Exploration and manufacturing corporations, as measured by the XOP ETF—which tracks the S&P Oil & Gasoline Exploration and Manufacturing Index—declined roughly 4%. Massive-cap built-in oil corporations held up higher: the XLE ETF fell solely about 1%. Oil service corporations had been the standout inside the sector, with the Philadelphia Oil Service Index advancing roughly 12.5% throughout the 12 months.

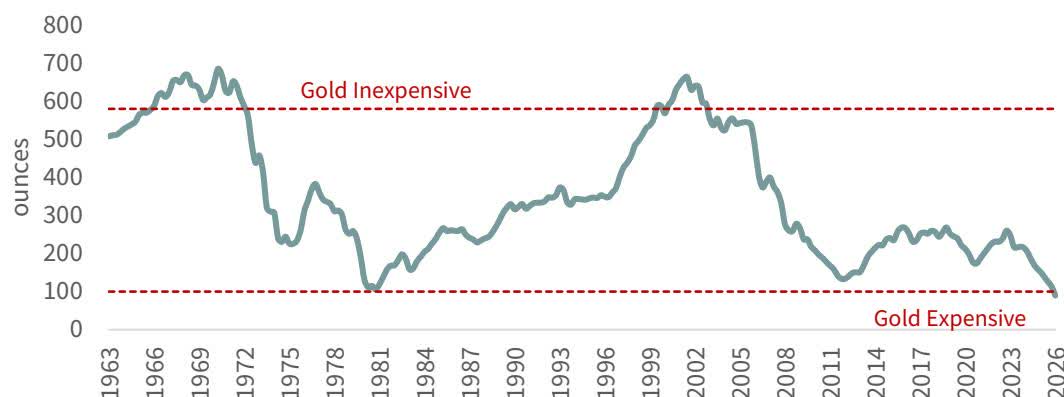

As oil costs drifted decrease all year long, investor sentiment towards the sector deteriorated into full despair. Nothing illustrates this despair extra clearly than oil’s valuation relative to gold. Previously 170 years, oil has been this low-cost relative to gold solely as soon as earlier than—throughout the top of the COVID-related panic in April 2020. At the moment the worldwide economic system had successfully shut down, Saudi Arabia had launched an ill-timed value warfare with Russia, and traders feared that international storage capability would actually overflow. Panic swept via oil markets, even forcing costs on the NYMEX futures alternate briefly into damaging territory as merchants rushed to exit contracts requiring bodily supply.

In our view, the Brent market supplied a extra consultant measure of situations on the time, provided that it’s cash-settled reasonably than bodily delivered. On April 21, 2020—when Brent costs reached their lowest level—one ounce of gold may buy roughly 87 barrels of oil, surpassing the earlier document of 48 barrels reached throughout the OPEC market-share warfare that resulted in early 2016, and solely six weeks in the past we nearly surpassed this COVID panic stage. On January twenty eighth, an oz of gold bought 86 barrels of oil—about 70% greater than the 2016 peak and just one barrel decrease than the acute ranges reached throughout the COVID panic of 2020.

What makes this comparability so placing is that underlying fundamentals in at the moment’s oil market bear little resemblance to the situations that prevailed in both 2015 or 2020. There aren’t any international COVID lockdowns suppressing demand, nor are there indicators that an OPEC market-share warfare is about to erupt. In each of these earlier intervals, provide considerably exceeded demand and international oil inventories had been rising quickly. Right this moment, in contrast, inventories have barely moved—a sign to us that the worldwide oil market is basically balanced reasonably than oversupplied.

In different phrases, oil’s near-record cheapness relative to gold seems to replicate excessive bearish sentiment reasonably than genuinely weak fundamentals. The disconnect between notion and actuality is exactly why we imagine at the moment’s oil market affords such compelling funding alternatives.

OIL’S NEAR-RECORD CHEAPNESS RELATIVE TO GOLD APPEARS TO REFLECT EXTREME BEARISH SENTIMENT RATHER THAN GENUINELY WEAK FUNDAMENTALS.

BY OUR ANALYSIS, OIL TODAY REPRESENTS THE CHEAPEST MAJOR ASSET CLASS IN THE WORLD.

Over the previous twenty-five years, international oil markets have undergone a whole reversal. Within the early 2000s, an oz of gold may buy solely about six barrels of oil—a ratio seen solely a handful of instances over the earlier 170 years. On the time, gold had turn into the “uninvestable” asset class—irrespective of how low the worth went it couldn’t be purchased. Right this moment the scenario has flipped. That very same ounce of gold now buys almost 13 instances as a lot oil, and now oil has turn into the brand new “uninvestable” asset class. Regardless of how low the worth goes–it can’t be purchased.

Twenty-five years in the past we argued that gold was the most affordable asset class on this planet and that it provided extraordinary alternative for traders keen to look past prevailing sentiment. Right this moment we’re making the identical case for oil. By our evaluation, oil is now the most affordable main asset class on this planet, and its valuation relative to gold strongly reinforces that conclusion. The alternatives rising in at the moment’s oil market, in our view, are substantial.

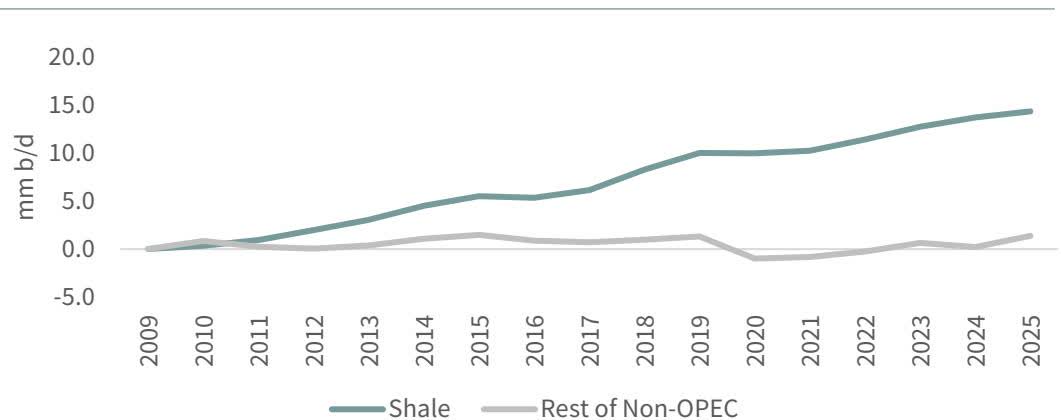

Vital constructive developments might quickly start to reshape the oil market, although few analysts seem centered on them at the moment. In our view, non-OPEC oil provide development is more likely to disappoint materially over the following a number of years—an end result whose significance can’t be overstated. Traditionally, the best competitor to OPEC manufacturing has all the time been non-OPEC provide. When international demand development exceeds the expansion of non-OPEC manufacturing, OPEC inevitably regains market share and pricing energy. This dynamic drove the highly effective oil bull markets of the Seventies and once more within the 2000s—and we imagine it’s starting to emerge as soon as extra.

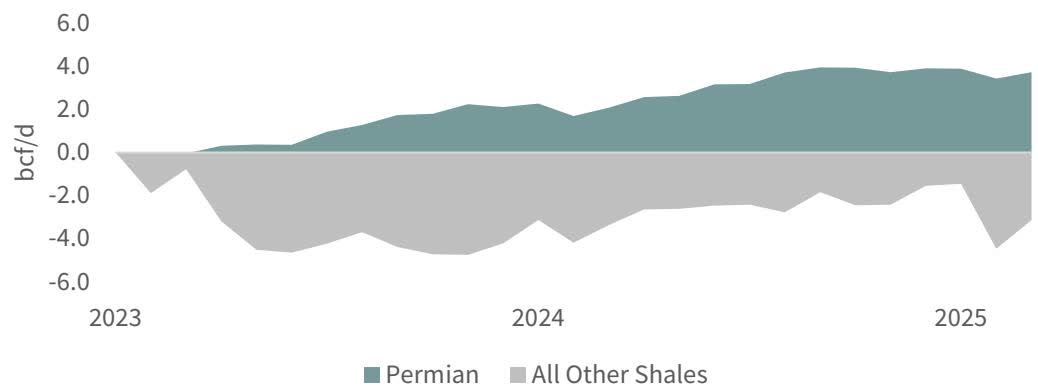

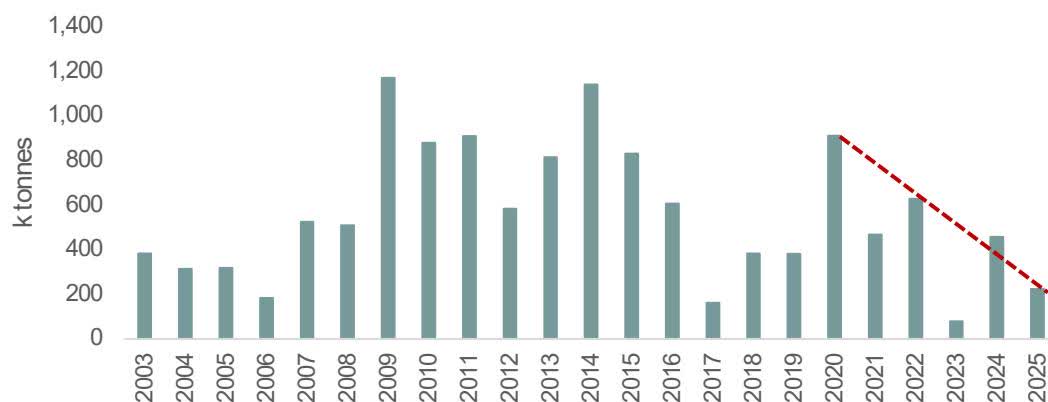

Over the previous fifteen years, roughly 80% of all non-OPEC provide development has come from U.S. shale manufacturing, as illustrated within the chart under.

FIGURE 7 Sources of Non-OPEC Manufacturing Development Since 2009

Supply: EIA.

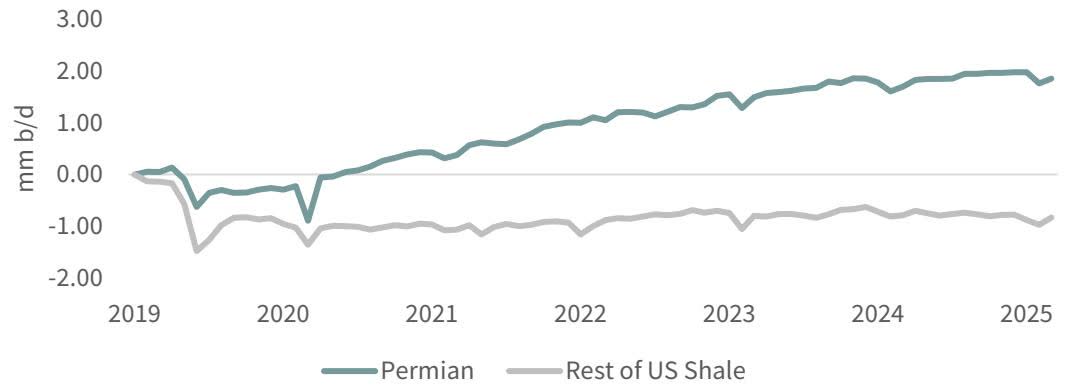

Outdoors of U.S. shale, non-OPEC provide development has been primarily nonexistent. The modest will increase which have occurred have come primarily from Canadian oil sands and biofuels. Equally essential are the altering dynamics inside the U.S. shale business itself. Since 2019, nearly all shale manufacturing development has come from a single basin—the Permian. Outdoors the Permian, shale manufacturing has successfully stagnated, as the next chart illustrates.

FIGURE 8 Shale Development since 2019

Supply: EIA.

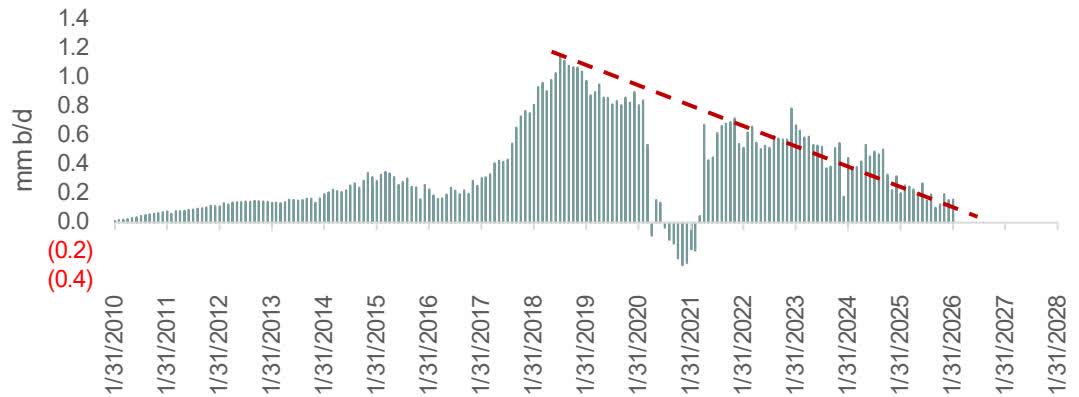

The ultimate piece of the non-OPEC slowdown story now seems to be falling into place. The Permian Basin—the final main supply of non-OPEC provide development—now seems to be approaching a plateau in manufacturing.

FIGURE 9 Permian Shale Oil Yr-on-Yr Development

Supply: EIA.

Pure Gasoline

North American pure gasoline was one of many few power markets to buck the prevailing bearish sentiment. U.S. pure gasoline costs rose roughly 12% throughout the quarter. Circumstances in Canada had been way more unstable. In September, Canadian spot pure gasoline costs briefly turned damaging as manufacturing continued to rise whereas the ramp-up of the nation’s new LNG export facility on the British Columbia coast proceeded extra slowly than anticipated. With restricted storage capability obtainable, producers had been pressured to pay consumers to take bodily gasoline off their fingers.

As colder winter climate arrived, nevertheless, costs recovered sharply. Canadian gasoline, which had successfully began the quarter close to zero, completed the interval round $2.00 per Mcf—a significant rebound. The episode of damaging pricing nonetheless strengthened the deeply bearish sentiment that has weighed on North American pure gasoline markets for a lot of the previous six months.

The energy in U.S. pure gasoline costs throughout the fourth quarter can largely be attributed to colder-than-normal climate. Temperatures had been roughly 10% under seasonal averages, significantly throughout December, which led to a pointy improve in storage withdrawals. The impression is clear when evaluating storage information throughout current years. Within the fourth quarter of 2023, roughly 175 bcf of gasoline was withdrawn from storage. Within the fourth quarter of 2025, withdrawals totaled roughly 310 bcf—almost double the prior stage.

Because of this, inventories coming into 2026 now sit solely modestly above their ten-year common. A lot of the bearish sentiment surrounding pure gasoline has been constructed on the belief that provide development will proceed to overwhelm demand. We imagine that narrative might quickly start to unravel.

Whereas current Vitality Info Administration (EIA) information present year-over-year manufacturing development, we imagine the underlying dynamics are extra nuanced. The newest surge in U.S. pure gasoline manufacturing successfully resulted in December 2023. Since then, complete dry gasoline provide has elevated by about 1.7 bcf per day. Shale manufacturing accounted for roughly 3.1 bcf per day of that development, implying that typical gasoline manufacturing truly declined by roughly 1.4 bcf per day over the identical interval.

Much more revealing is the supply of the remaining shale development. Since December 2023, manufacturing from the Permian Basin has risen by roughly 3.7 bcf per day, whereas manufacturing from all different shale basins has declined by about 0.6 bcf per day. In different phrases, not solely has primarily all current development in U.S. pure gasoline provide come from shale formations, however almost all of that development has been concentrated in a single area—the Permian Basin, as illustrated within the chart under.

FIGURE 10 Sources of Shale Gasoline Development since 2023

Supply: EIA.

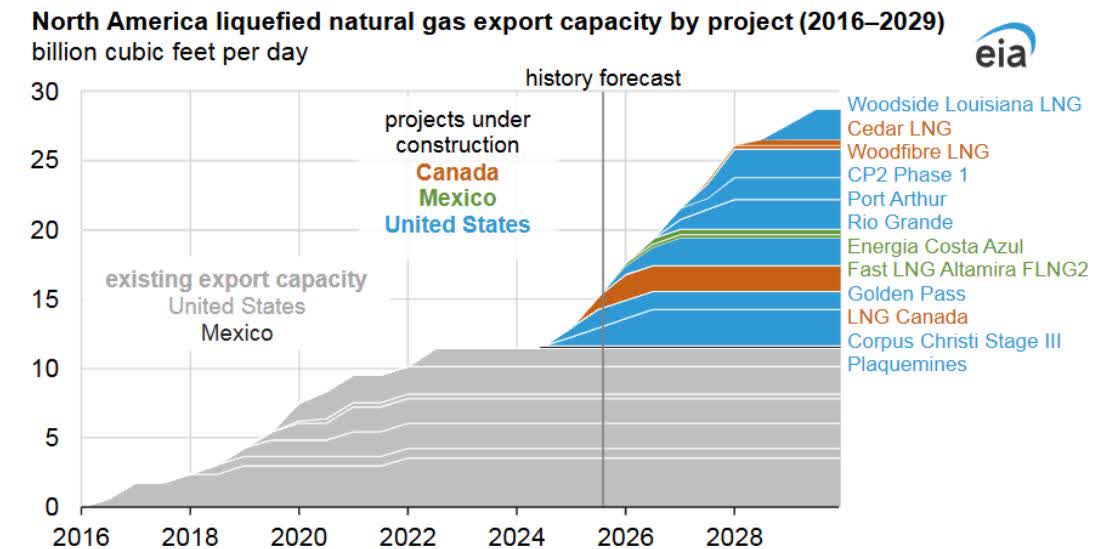

We imagine that after the Permian’s present “gasoline burp”—a topic we mentioned in our final letter—runs its course, gasoline provide development from the basin will start to plateau and finally decline. Oil manufacturing development within the Permian has already slowed markedly, and we anticipate pure gasoline provide to comply with an analogous trajectory over the following six to 12 months. As provide development slows and demand for North American LNG continues to develop, the stability within the gasoline market ought to tighten considerably—setting the stage for materially greater pure gasoline costs.

FIGURE 11 US LNG Export Capability

Information supply: U.S. Vitality Info Administration, Liquefaction Capability File , and commerce press

As we write, pure gasoline costs have already begun to rise in response to longer-range forecasts calling for considerably colder-than-normal temperatures throughout a lot of america. We subsequently suggest that traders keep their publicity to pure gas-related investments. At current, many pure gasoline equities look like valued utilizing an assumed gasoline value of roughly $3.50 per Mcf—a stage that, in our view, will probably show far too conservative in hindsight.

Uranium

Uranium markets had been comparatively quiet throughout the fourth quarter. Spot costs had been largely unchanged, ending the quarter close to $82 per pound. Time period costs—these utilities pay when contracting for long-term provide—continued to maneuver greater. In keeping with information reported by Cameco (CCJ), time period costs rose roughly 7% throughout the quarter to $81.55 per pound, narrowing the hole with spot costs, which ended the quarter at $81.60.

In our earlier letter, we outlined two highly effective forces that we imagine will drive uranium costs considerably greater within the years forward: continued development in demand from nuclear energy technology and the mounting threat of provide disappointments throughout the uranium mining business. The World Nuclear Affiliation strengthened this view in its broadly adopted World Nuclear Efficiency Report 2025 . In that report, the WNA raised its projection for international nuclear energy technology in 2040 by roughly 10% in contrast with estimates revealed simply two years earlier. The upward revision displays each the extension of working lives for present reactors and a rising pipeline of latest nuclear capability beneath improvement.

On the gasoline facet, the implications are substantial. The WNA estimates uranium demand will improve from roughly 179 million kilos in 2025 to roughly 330 million kilos by 2040—a rise of about 85% over present ranges.

Along with discussing the outlook for demand, we additionally highlighted the rising threat of provide disappointments that would emerge between now and 2030. Within the Uranium part of this letter, we look at how the current difficulties encountered on the just lately restarted Honeymoon uranium undertaking in Australia present a transparent instance of the sorts of operational challenges which will more and more have an effect on uranium mine provide within the years forward.

We additionally evaluate a number of high-profile developments that reinforce our thesis of strengthening nuclear-powered uranium demand. Lastly, we focus on the re-emergence of investor demand for bodily uranium—a steadily neglected however probably highly effective supply of demand. Investor accumulation performed an essential function throughout the first leg of the uranium bull market, and we imagine that this demand supply has begun to reappear over the previous six months.

Agriculture

Grain and fertilizer markets had been comparatively quiet throughout the fourth quarter because the North American harvest season got here to an in depth.

Grain costs had been blended. Corn and soybean costs rose 4% and 1%, respectively, whereas wheat costs declined 2%. Fertilizer costs confirmed a usually downward bias: urea rose modestly by 3%, however potash costs fell 7% and phosphate costs declined by greater than 20%. Grain markets at the moment are approaching their fifth 12 months of a bear market. Since peaking within the spring of 2022, wheat, corn, and soybean costs have fallen between roughly 45% and 65%. Over the course of this extended decline, pessimism amongst grain merchants has reached extraordinarily elevated ranges.

In 2024, speculative merchants in corn, soybeans, and wheat established essentially the most bearish positioning seen in additional than thirty-five years of knowledge. On the identical time, industrial members in these markets moved in the wrong way, constructing important lengthy positions. Traditionally, this mix—document bearish positioning by trend-following speculators alongside bullish positioning by industrial members, typically thought-about the market’s “good cash”—has steadily signaled {that a} main bear market could also be approaching its finish.

Though we have now not but seen a decisive reversal, grain costs have begun to edge regularly greater—even within the face of still-bearish basic information. Since speculative merchants established their document bearish positions, corn, wheat, and soybean costs have risen between roughly 10% and 25%. Given the repeated bullish alerts rising from grain market positioning over the previous twelve months, we imagine a serious backside in international grain markets might already be forming. Within the close to time period, nevertheless, basic situations counsel that the bear market in grains may persist considerably longer.

Essentially the most bearish information presently comes from the U.S. corn market. In its preliminary estimate for the 2025–2026 crop 12 months, the U.S. Division of Agriculture’s World Agricultural Provide and Demand Estimates (WASDE) projected corn ending shares of roughly 1.8 billion bushels—putting inventories within the higher quartile of observations over the previous thirty years. We imagine, nevertheless, that the market may in the end comply with a sample just like what occurred in Might 2024. At the moment, the USDA initially projected very massive 2024–2025 ending shares of roughly 2.1 billion bushels. Nevertheless, a scorching and dry summer season lowered yields, whereas export demand proved stronger than anticipated. Because of this, ending shares had been finally revised right down to roughly 1.5 billion bushels—a a lot tighter and extra supportive stock stage.

Had the new, dry situations of the summer season of 2024 repeated in 2025, the comparatively tight corn inventories coming into the 12 months would probably have produced important upward strain on costs. As an alternative, the other occurred. The 2025 rising season proved broadly favorable, with regular temperatures and precipitation throughout a lot of the U.S. Corn Belt.

Preliminary USDA projections had farmers harvesting roughly 87.4 million acres of corn with a mean yield of 181 bushels per acre, producing a crop of about 15.8 billion bushels. In its most up-to-date estimates, nevertheless, the USDA now believes farmers harvested roughly 91.3 million acres with a document common yield of 186.5 bushels per acre, leading to a crop barely above 17 billion bushels. Though corn utilization and exports elevated meaningfully, the surge in manufacturing greater than offset these beneficial properties. Because of this, corn ending shares have risen to just about 2.2 billion bushels—a stage that continues to be basically bearish for costs. For corn markets to maneuver materially greater in 2026, climate situations throughout the upcoming planting and rising season will probably want to show considerably much less favorable.

In soybeans, the underlying basic image is considerably extra constructive. Preliminary projections for the 2024–2025 soybean crop positioned ending shares at roughly 445 million bushels—ranges that ranked within the high 20% of observations over the previous thirty-five years. Nevertheless, the identical scorching and dry situations that affected components of the rising season additionally weighed on soybean yields. The USDA initially projected that farmers would harvest roughly 85.6 million acres of soybeans with a document yield close to 52 bushels per acre. Newer estimates point out that farmers planted about 86.2 million acres, however yields in the end got here in decrease, averaging roughly 50.7 bushels per acre.

Because of this, the USDA revised its estimate of the 2024 soybean harvest from about 4.45 billion bushels to roughly 4.37 billion bushels. That discount lowered 2024–2025 ending shares to roughly 325 million bushels—a significantly much less bearish stock stage.

For the 2025–2026 crop 12 months, the USDA initially projected ending shares close to 295 million bushels, representing a modest enchancment relative to the prior 12 months. Early forecasts assumed that farmers would harvest roughly 82.7 million acres with a mean yield of about 52.5 bushels per acre, producing a crop of roughly 4.34 billion bushels. In its most up-to-date WASDE replace, nevertheless, the USDA lowered its estimate of harvested acreage to round 80.4 million acres whereas barely elevating the anticipated yield. The revised estimates indicate a soybean crop of roughly 4.26 billion bushels—almost 100 million bushels decrease than earlier projections.

Essentially the most important revisions, nevertheless, have occurred within the USDA’s projections for soybean exports. Ongoing commerce tensions have led China to cut back imports of U.S. soybeans. The USDA had initially projected U.S. soybean exports at roughly 1.815 billion bushels for the 2024–2025 advertising and marketing 12 months. In its most up-to-date replace, nevertheless, the company lowered that estimate to roughly 1.575 billion bushels. Because of this, projected soybean ending shares for the 12 months have elevated to roughly 350 million bushels—a list stage that continues to be modestly bearish.

Taken collectively, the comparatively massive corn inventories and the considerably elevated soybean shares counsel that grain costs might proceed to commerce sideways within the close to time period, not less than till clearer alerts emerge from Northern Hemisphere planting situations in 2026.

Over the long term, we stay constructive on international grain markets. We proceed to imagine that climate patterns in a number of of the world’s main grain-producing areas are coming into a interval of accelerating stress—situations that we imagine could also be linked to the Gleissberg sunspot cycle, a topic we have now mentioned intimately in earlier letters. As proof that this cycle might already be influencing international agricultural situations, we have now included maps exhibiting subsurface soil moisture ranges throughout North America, Europe, and South America. These maps, revealed by NASA, point out that every one three areas proceed to expertise persistent moisture deficits.

Regardless of these longer-term considerations, we imagine that above-average grain inventories will probably delay the present bear market. Now in its fourth 12 months, the downturn in grain costs might subsequently proceed for a while earlier than the tighter provide situations implied by these climate patterns start to say themselves.

FIGURE 12a Drought Circumstances

Supply: NASA Grace.

FIGURE 12b Drought Circumstances

Supply: NASA Grace.

Coal

Coal costs moved modestly greater globally throughout the fourth quarter. In america, Powder River Basin thermal coal rose 2%, Appalachian coal elevated almost 4%, and Illinois Basin coal superior about 5%. Worldwide costs additionally strengthened barely, with Newcastle thermal coal gaining simply over 1% and Richards Bay costs rising 2%.

Coal equities continued their regular advance as nicely. The Dow Jones U.S. Coal Inventory Market Index—one of many few remaining indices that also tracks coal producers—rose roughly 5% throughout the quarter. For the complete 12 months, coal shares dramatically outperformed the broader fairness market, gaining roughly 65% in contrast with an 18% rise within the S&P 500.

Regardless of this robust efficiency, investor curiosity in coal equities stays extraordinarily restricted. For the reason that starting of the present commodity bull market—utilizing January 1, 2020 as a place to begin—coal shares have risen roughly 275%. That efficiency far exceeds the returns of each pure useful resource equities, which have gained about 143% as measured by the S&P North American Pure Useful resource Sector Index, and the broader fairness market, the place the S&P 500 has risen roughly 132%. As we have now famous in earlier letters, coal equities have traditionally led each main commodity bull market over the previous 130 years, and the present cycle seems to be following that very same sample.

Regardless of the shortage of investor curiosity, constructive developments proceed to emerge within the coal sector. Proof is mounting that the lengthy wave of coal plant closures in america might lastly be approaching an finish. Since 2010, roughly 390 coal-fired energy vegetation have both been shut down or scheduled for closure, leaving fewer than 200 vegetation presently working. Because of this, U.S. thermal coal consumption has fallen dramatically—from a peak of almost 1.1 billion tons in 2008 to an estimated 370 million tons by 2024, a decline of roughly 70%.

Nevertheless, 2025 seems to have introduced an surprising shift. Coal consumption is estimated to have risen by roughly 7% to eight% throughout the 12 months, supported by greater pure gasoline costs and rising electrical energy demand—significantly from energy-intensive information facilities. Coal-fired electrical energy technology itself elevated by roughly 13% in 2025. Most analysts have interpreted this rebound as a brief deviation inside a longer-term decline, viewing it as little greater than a one-year interruption in what has in any other case been a gentle downward development.

Latest developments, nevertheless, are starting to problem that broadly held view. It now seems that not less than 15 to 16 coal-fired energy vegetation that had been scheduled for closure someday after 2026 have both had their retirements delayed or cancelled. Supporting these choices has been a collection of emergency orders issued by U.S. Vitality Secretary Wright beneath the Federal Energy Act, requiring sure vegetation to stay operational past their deliberate retirement dates. On February 17, Secretary Wright issued his fourth such order, directing that the J.H. Campbell coal-fired plant in Michigan—initially scheduled to shut on Might 31, 2025, roughly fifteen years earlier than the tip of its anticipated working life—stay open. Shortly after this announcement, the Tennessee Valley Authority (TVA) additionally indicated that it could pause the deliberate retirement of two of its largest coal-fired amenities. These actions counsel a rising coverage shift geared toward sustaining coal-fired technology to help grid reliability and comprise electrical energy prices.

The fast development in electrical energy demand from synthetic intelligence and information heart infrastructure has been cited as a key issue behind these choices. Over the previous fifteen years, the closure of U.S. coal-fired vegetation has performed a serious function in lowering international coal consumption. If these closures now sluggish or reverse, it could characterize an essential shift within the international coal outlook. Early indicators counsel that U.S. coal consumption might have stabilized and will even be starting to develop once more—an essential constructive improvement for the worldwide coal business that has largely gone unnoticed by the few analysts who nonetheless comply with the sector carefully.

Outdoors america, coal fundamentals additionally proceed to strengthen. In earlier letters we mentioned how mounting proof means that coal is turning into more and more embedded in China’s long-term electrical energy technique. Many power analysts—together with the Worldwide Vitality Company—have repeatedly argued that China’s coal demand has already peaked and that renewable power will quickly start changing coal because the nation’s dominant gasoline supply. Whereas this end result might align with the aspirations of many power policymakers, the obtainable information proceed to level in a really completely different path.

In that context, we learn with specific curiosity a Bloomberg article revealed on December 10, 2025 titled, “Techniques to Dump Coal Are Failing in Asia as Vitality Demand Booms: Coal’s Grip on Asia Strengthens as Early Phaseout Bid Stalls.”

In that article, the Bloomberg reporter states: “Coal’s future is wanting vibrant, because the top-consuming area’s efforts to shift to scrub power endure a collection of setbacks.” The article factors out that China added 80 gigawatts of latest coal-fired producing capability in 2025, the very best stage in a decade, with equally capability additions scheduled for each 2026 and 2027. The article additionally highlights that India stays dedicated to rising its coal-fired electrical energy producing capability by 87% by 2047—an estimated improve of just about 420 gigawatts.

And at last the article highlights how Indonesia continues to take a position closely in coal fired power capability whereas persevering with to delay its promised retreat from coal-fired energy technology. The Indonesian authorities, for instance, has cancelled plans to retire the large Cirebon-1 coal fired plant in West Java. Indonesian officers mentioned the choice to maintain the plant open was made as a result of Cirebon’s working life stays intensive, and that promised United Nation’s funding for the plant’s closure had not been forthcoming.

NO GLOBAL INDUSTRY HAS BEEN MORE CAPITAL STARVED.

We’ve lengthy held that slowing the expansion in Asia coal consumption, though a laudable purpose, may by no means be achieved given the power necessities of the area. Echoing this line of reasoning, the Bloomberg article quotes Jim Madan, a Wooden Mackensie analyst who says: “…It comes down to produce safety and prices. Even with document wind and photo voltaic build-outs, new additions are nonetheless not retaining tempo with large improve in energy demand from inhabitants development, rising incomes and now the surge in information heart capability—that hole is being crammed by fossil fuels like and gasoline.” In earlier letters, we have now mentioned these exact same points, and got here up with the exact same conclusions.

Coal inventory are low-cost, and we imagine that they’re about to renew management standing each in relations to the overall shares market, and to pure useful resource shares as nicely. For those who have the flexibility to take a position, we might use any weak spot as a possibility to extend publicity. Coal costs have declined on common by 70% since they peaked mid 2022 in response to Russia invasion of Ukraine. No international business has been extra capital starved, and coal demand continues to shock to the upside. A brand new bull market in coal costs, we imagine has begun.

Surging Uranium Demand Meets a Fragile Provide Base

Since our final letter, one other provide disappointment has emerged in international uranium markets. Whereas the volumes concerned are comparatively small, the event illustrates a broader level: the sorts of operational and technical difficulties which might be more likely to plague uranium mine provide development within the years forward.

In December, Boss Vitality introduced a major setback at its flagship Honeymoon uranium mine, main the corporate to withdraw its 2021 “Enhanced Feasibility Research” (EFS). That examine had projected manufacturing ramping to roughly 2.4 million kilos yearly over a fifteen-year mine life, with a subsequent growth probably lifting output to three.3 million kilos per 12 months.

Since restarting manufacturing in 2024, nevertheless, the undertaking has skilled materials deviations from assumptions underlying the unique examine. The corporate now expects annual manufacturing of solely about 1.5 million kilos, with the mine’s life more likely to be considerably shorter than initially anticipated.

The Honeymoon mine had beforehand closed in 2013, and its restart was broadly seen as an indication that Australia’s uranium business was returning to development. That optimism now seems untimely. The frustration at Honeymoon affords a vivid instance of how troublesome it might show to develop uranium mine provide sufficiently to fulfill the surge in demand that lies forward.

On the demand facet, constructive developments proceed to speed up. Within the third quarter, Google (GOOGL), Kairos Energy, and the Tennessee Valley Authority introduced a serious collaboration centered on a novel energy buy settlement. Underneath the association, Kairos Energy’s Hermes 2 reactors will ship electrical energy into the TVA grid, in the end supplying energy to Google’s information facilities in Tennessee and Alabama.

The settlement requires as much as 50 megawatts of energy to be delivered from these reactors, marking the primary time a U.S. utility has contracted to buy electrical energy generated by a sophisticated “Gen IV” nuclear reactor. It additionally represents the primary deployment beneath the broader partnership between Google and Kairos Energy introduced in 2024, an initiative that in the end goals to produce roughly 500 megawatts of nuclear-generated electrical energy to help Google’s rising power necessities. These Hermes reactors shall be constructed beneath permits issued by the U.S. Nuclear Regulatory Fee (NRC).

Relating to additional constructive information relating to SMR’s and the NRC, Terra Energy, one other chief within the improvement of sodium primarily based SMR’s, acquired notification from the NRC that they had been issued the primary ever development allow to construct a sophisticated, commercial-scale nuclear energy plant. The Terra Energy SMR shall be in-built Wyoming, and is scheduled to return on line in 2030. Terra Energy, backed by Invoice Gates, is a frontrunner within the improvement of sodium-based SMR’s, and Their “Natrium” reactor, is being developed via the united statesDepartment of Vitality’s Superior Reactor Demonstration program, and it is going to be the primary utility scale superior nuclear energy plant to be in-built america.

Each these developments, In our view, ship a powerful sign that salt-based small modular reactor applied sciences are quickly gaining significant acceptance.

Google adopted this announcement with one other important step ahead. On October 27, Google and NextEra Vitality (NEE) introduced plans to restart the Duane Arnold Vitality Middle, a 600-megawatt nuclear facility that had been shut down in 2020. Underneath the settlement, Google will buy the plant’s energy output via a 25-year contract, whereas the 2 corporations can even discover broader deployment of nuclear technology nationwide to help Google’s increasing power wants. The Duane Arnold plant is presently scheduled to restart operations in 2030.

By far essentially the most intriguing—and probably most essential—announcement got here shortly after the quarter ended. On January 9, Meta Platforms (META) unveiled a brand new settlement with Vistra (VST)—the most important generator of aggressive electrical energy in america—in addition to with TerraPower and Oklo (OKLO).

The announcement builds on Meta’s settlement final 12 months with Constellation Vitality (CEG) and positions the corporate to turn into one of many largest company purchasers of nuclear-generated electrical energy in america.

The settlement features a 20-year energy buy association beneath which Vistra will provide electrical energy to Meta Platforms from a number of presently working nuclear amenities, together with the Perry Nuclear Energy Plant and the Davis-Besse Nuclear Energy Station, in addition to the Beaver Valley Nuclear Energy Station.

As well as, TerraPower will fund and help the event of as much as eight of its Natrium molten-salt-based reactors. Underneath the plan, TerraPower will initially ship two reactors able to producing roughly 690 megawatts of electrical energy by 2032, together with choices for six further reactors able to producing a mixed 2.1 gigawatts of energy, focused for deployment by 2035.

The announcement additionally included plans for Oklo—with monetary backing from Meta—to put in roughly 1.2 gigawatts of capability utilizing Oklo’s Aurora small modular reactor know-how. These reactors are anticipated to be deployed at Meta’s deliberate information heart campus in Pike County, Ohio, which is presently scheduled to start operations round 2030.

Meta’s announcement carries a number of essential implications. The Davis-Besse Nuclear Energy Station, Perry Nuclear Energy Plant, and Beaver Valley Nuclear Energy Station had been initially scheduled for decommissioning in 2020 and 2021. These closures had been averted solely after each the Ohio and Pennsylvania state legislatures supplied monetary help to maintain the amenities working.

When the vegetation had been acquired by Vistra in 2023, their long-term futures remained unsure. Following Meta’s settlement, nevertheless, Vistra has indicated that the outlook for all three vegetation is now safe. The corporate is pursuing license extensions of as much as twenty years, which may permit these reactors to proceed working for so long as one other thirty years.

When the World Nuclear Affiliation considerably raised its uranium demand estimates in its 2025 examine, it emphasised that extensions of present nuclear energy plant working lives can be a serious contributor to future demand—an remark that’s nicely supported by Meta’s current bulletins.

In the meantime, the restart of Japan’s nuclear business continues to assemble momentum. This month, Tokyo Electrical Energy Firm restarted Unit 6 on the Kashiwazaki-Kariwa Nuclear Energy Plant. Japan has now restarted fifteen of the fifty-four reactors that had been shut down following the Fukushima nuclear catastrophe, with one other ten reactors presently transferring via the restart course of. Nuclear energy presently accounts for roughly 10% of Japan’s electrical energy technology, however the authorities has made clear its intention to lift that determine to roughly 20% within the years forward.

Japan has additionally shifted its official power coverage towards “maximizing the usage of nuclear energy” as a way to meet rising electrical energy demand—significantly from synthetic intelligence infrastructure and information facilities. The plan not solely entails restarting idle reactors but additionally constructing the following technology of nuclear vegetation. The federal government is encouraging development of each large-scale reactors and small modular reactors (SMRs). For instance, Kansai Electrical Energy just lately introduced plans to assemble a next-generation reactor at its present Mihama Nuclear Energy Plant web site.

Taken collectively, these developments counsel that the trajectory of utility-driven uranium demand continues to steepen. On the identical time, the approaching surge in utility demand might quickly collide with a revival of investor demand for bodily uranium.

When Sprott Asset Administration took over the previous Uranium Participation Company in July 2021 and relaunched it because the Sprott Bodily Uranium Belief (SPUT), uranium costs had been buying and selling close to $32 per pound and the belief held roughly 18.2 million kilos of uranium. Over the next two and a half years, the belief acquired roughly 45 million kilos within the open market—a lot of it representing the final remaining surplus stock left over from the Fukushima period and nonetheless held by utilities and speculators. The return of each industrial and investor demand helped push uranium costs to $106 per pound, which in hindsight seems to have marked the tip of the primary leg of the uranium bull market.

Following that January 2024 peak, investor demand retreated alongside the declining uranium value. Throughout the eighteen months that adopted, the Sprott belief bought solely about 3 million further kilos, providing little help to a uranium market that noticed costs fall roughly 40%, from $106 to $65 per pound.

Nevertheless, after resolving its liquidity constraints in June 2025, the Sprott Bodily Uranium Belief (SPUT) has as soon as once more returned as an lively purchaser within the bodily uranium market. For the reason that finish of June, the belief has bought roughly 10 million kilos of uranium within the open market, bringing its complete holdings to roughly 77.4 million kilos. We discover it unlikely to be a coincidence that uranium costs have surged roughly 45% over the previous seven months as investor demand has re-emerged. As we have now emphasised in earlier letters, investor participation within the bodily uranium market is more likely to play a serious function in figuring out uranium costs within the years forward, and the renewed accumulation of stock is one other sign that costs could also be headed considerably greater.

On the identical time, nuclear flora extensions, reactor restarts, and new development are all contributing to an more and more steep demand trajectory. But the nuclear business lacks the deep pipeline of latest uranium initiatives required to fulfill this future demand. Even the initiatives presently beneath improvement will nearly actually encounter delays and operational disappointments—one thing nicely illustrated by the underwhelming restart of the Honeymoon uranium mine in Australia. That undertaking was initially anticipated to provide roughly 3 million kilos of uranium yearly for fifteen years; it now seems more likely to produce solely about half that quantity and for a a lot shorter mine life.